The Boeing Company 401(k) Retirement Plan: Deferred Compensation

Boeing has over $60 billion in plan assets amongst ~200,000 participants, easily making it one of the largest retirement plans in the US.

Employer matches, immediate vesting, Post-tax and Roth 401(k) contributions are all benefits offered in Boeing’s 401(k) plan.

Boeing VIP Transition Guide: January 2022

DISCLOSURE: McIlrath & Eck is not affiliated with The Boeing Company. While McIlrath & Eck communicates with its clients and educates itself regarding employee benefits, there is no guarantee that the information provided is accurate. The information is provided for informational purposes only, and it should not solely be relied upon for investment decisions. Employees of The Boeing Company should contact their HR representative regarding specific benefits.

Contributions

Tax Treatment: Tax paid at distribution

Tax Treatment of Earnings: Taxed at distribution

Contribution Limits: $24,500 ($32,500 50+ catch-up) ($35,750 60-63 catch-up)

Employer Match: Qualify for employer-matching contributions

Incentive Contributions: A separate election may be for a portion or all of an incentive payment

- Pre-tax contributions allow an employee to lower their taxable income during their working years, and pay income taxes on their withdrawals in retirement when they’re likely in a lower tax bracket.

Tax Treatment: Tax paid at contribution

Tax Treatment of Earnings: Taxed at distribution

Contribution Limits: No “limit” per se, though contributions cannot exceed IRS annual additions limit of $72,000 ($80,000 50+) (Employee & Employer combined) *50+ catchup not available*

Employer Match: Qualify for employer-matching contributions

Incentive Contributions: Not available

- Post-tax contributions are a great way for high-income earners to save extra amounts for retirement if their contribution and employer match has not reached the $72,000 ($80,000 50+) limit.

Tax Treatment: Tax paid at contribution

Tax Treatment of Earnings: Not taxed if a qualified distribution

Contribution Limits: $24,500 ($32,500 50+ catch-up) ($35,750 60-63 catch-up)

Employer Match: Qualify for employer-matching contributions

Incentive Contributions: A separate election may be made for a portion or all of an incentive payment

- Roth contributions allow for tax-free withdrawals in retirement, with all earnings growth being tax-free as well. After-tax 401(k) funds may be used to take advantage of a ‘Mega Backdoor Roth Conversion’

Investment Options

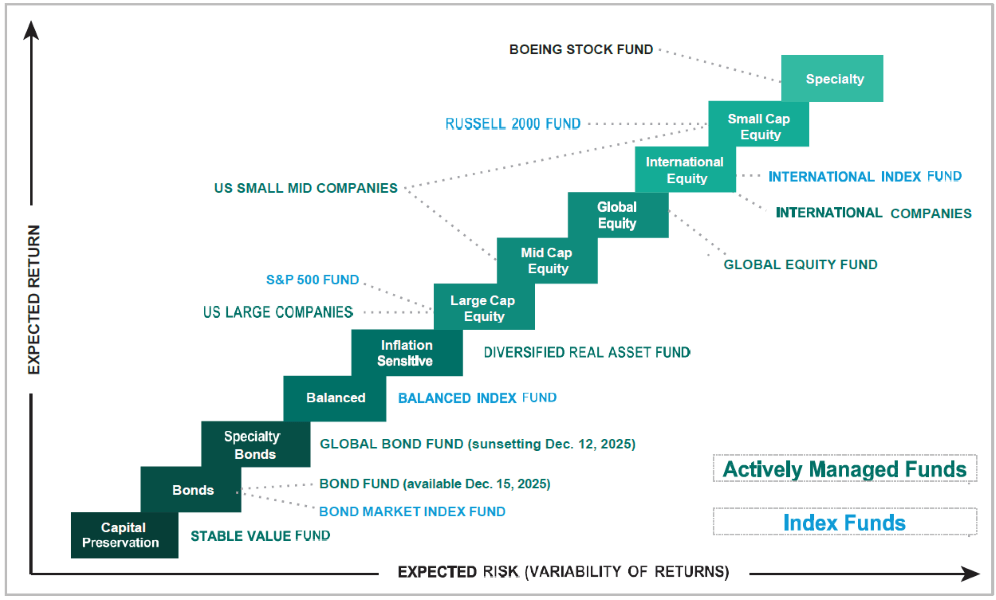

Lifecycle Funds, Index Funds, Actively Managed Funds, and a Company Stock Fund are all available investment options in Boeing’s 401(k) plan. Choosing an investment allocation that aligns with an individual’s tolerance and capacity for risk while doing so in low-cost investments is paramount to long-term success.

- Lifecycle Funds: also referred to as “Target date” funds, these investments offer a diversified mix of asset classes combined into a single fund. Management of the exposure to different asset classes is at the discretion of the fund manager.

- Index Funds: Passively managed funds, whose goal is to track the performance of a broader index (i.e. S&P 500 index, Russell 2000, etc.). Without active management, these funds offer considerably lower fees compared to more closely managed funds.

- Actively managed Funds: As the name implies, a manager selects individual securities to buy and sell within the fund according to the constraints of the fund’s prospectus.

- Retirement Fund

- 2030 Fund

- 2035 Fund

- 2040 Fund

- 2045 Fund

- 2050 Fund

- 2055 Fund

- 2060 Fund

- 2065 Fund

- Bond Market Index Fund

- Balanced Index Fund

- S&P 500 Index Fund

- International Index Fund

- Russell 2000 Index Fund

- Stable Value Fund

- Bond Fund

- Diversified Real Asset Fund

- U.S. Large Companies Fund

- Global Equity Fund

- International Companies Fund

- U.S. Small/Mid Companies Fund

- Boeing Stock Fund

View the details of the investment options here.

Current Union-Represented Employees and BAO C2 | Update

Source: Boeing Company Investment Guide

Pension Value Plan (PVP)

The PVP is a Defined Benefit Cash Balance Pension Plan, providing a monthly benefit based upon years of credited service and compensation for roughly 68,000 non-union employees

A ‘Cash Balance’ pension plan contains hypothetical individual accounts that are credited with a dollar amount for each employee

This plan is frozen, meaning some or all workers who are currently covered under the plan will no longer experience increases in the value of their pension. New employees who are not already participating in the PVP will not be allowed to enter the plan.

Benefits are payable in the form of an annuity (Single life, 50% survivor, 75% survivor, etc.) or as a one-time lump sum payment.

| To elect a benefit commencement date of: | All paperwork must be properly completed and received by: | If so, your pension payments are expected to start on or around: |

| May 1, 2022 | April 30, 2022 | June 1, 2022 |

| June 1, 2022 | May 31, 2022 | July 1, 2022 |

| July 1, 2022 | June 17, 2022 | Aug. 1, 2022 |

| Aug. 1, 2022 | July 31, 2022 | Sept. 1, 2022 |

| Sept. 1, 2022 | Aug. 31, 2022 | Oct. 1, 2022 |

Source: https://boeingretirementchanges.com/pension-plans-current-vested-employees

The Boeing Company Employee Retirement Plan (BCERP)

Boeing’s BCERP is a Defined Benefit Pension Plan, providing participants with a monthly retirement benefit calculated using years of credited service and compensation

Benefits accrued under the BCERP are primarily pay related

Benefits are payable in the form of an annuity (Single life, 50% survivor, 75% survivor, etc.) or as a one-time lump sum payment.

Pension Plan Updates:

Lump Sum V. Monthly Benefit Analysis

There is no “one size fits all” when determining which pension benefit option is most optimal for a retiree. Careful financial planning analysis and an in-depth look at an individual’s situation should be undertaken before selecting a benefit option. Choosing how to receive your pension benefit is an irreversible decision that should not be taken lightly, all aspects of an individual’s life should be considered.