Plan for now, prepare for the future. Get ready for 2021!

The year 2020 was a brutal one for the economy and for our daily lives. The pandemic caused a strong downturn, and unemployment spiked in the spring. Economic conditions have only just started to turn around. So how fast will things get back to normal? Here’s a high-level look at the forces that will shape the economy and markets in 2021.

The course of the pandemic will be key

McIlrath & Eck’s economic outlook for 2021 is based on positive coronavirus-related health outcomes for the broader population. If consumers start resuming travel, entertainment, and other consumer activities, the economy can get back into gear. A healthy economy begins and ends with a healthy population. But the recovery is likely to be uneven, with face-to-face sectors such as restaurants likely the last to fully recover.

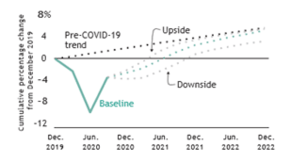

Health outcomes drive next phase of recovery.

Notes: The y-axis represents the GDP-weighted level impact from the baseline, which is December 2019 for major global economies. The teal and gray dotted lines represent three forecasts: our base case and upside and downside scenarios. The downside scenario is characterized by a failure to significantly reduce virus transmission in the short term, which would cause a slower recovery. Potential problems with the efficacy, adoption, distribution, or safety of a vaccine could also surface. The upside scenario is characterized by a speedy, large-scale distribution of an effective vaccine, which will see the economy return to normal more quickly than we currently expect. Sources: Vanguard and Refinitiv, as of November 30, 2020.

Growth is expected to begin making up for lost ground

- The hit we saw to the global economy in early 2020 was the largest since World War II, but the early pace of recovery has also been sharp.

Economies around the world are continuing on their paths to recovery. We see this second phase of the recovery playing out over the next year or two as businesses and consumers regain a sense of normalcy.

China has made swift return to near pre-pandemic output, and we see that extending in 2021 with growth of around 9%. We expect growth of approximately 5% in the U.S. and 5% in the euro area, with those economies ending at or marginally below their pre-pandemic output levels. In emerging markets, we expect an uneven and challenged recovery, with an aggregate growth of about 6%.

Inflation should be tame, and the job picture is set to improve

Some worry that rising debt levels from stimulus packages may cause inflation levels to soar. We see the potential for a bump in inflation early in the year, but we don’t expect that to be sustained. Inflation will likely end the year below 2%, though we air on the side of conservatism with a regular rate of 4.28% used in our financial plans. As the health picture improves in the second half of 2021, look for a sharp acceleration in job growth, and an unemployment rate near 5% at the end of 2021.

Market returns may be modest

Our outlook for global asset returns is guarded. This is most true for stocks, as high valuations and lower economic growth rates mean you can expect lower returns over the next decade. Possible bright spots: international and value stocks, which have been laggards for years. Our preference in value weighted stocks, mutual funds and passively managed ETFs have not seen the fiery returns that many growth-oriented funds have experienced of late, though our favoritism in value is often rewarded with less volatility and an increased probability of investing in financially sound and undervalued companies.

Given the strong, if not uniform, recovery in global stock prices, the risk of a sharp downturn (defined as a greater than 20% drop) over the next three years remains elevated.

For bonds, lower interest rates and flatter yield curves (where there’s not a lot of difference between short-, mid-, and long-term rates) are expected to weigh on returns for the foreseeable future. But instead of viewing this asset class as a primary return-generating investment, think of bonds more from a diversification and risk-mitigating perspective.

There is no guarantee investment strategies will be successful. Investing involves risks including possible loss of principal. Diversification does not eliminate the risk of market loss.

All expressions of opinion are subject to change. This article is distributed for informational purposes, and it is not to be construed as an offer, solicitation, recommendation, or endorsement of any particular security, products, or services